The 17th BRICS Summit is being held from July 6 to 7 in Rio de Janeiro, Brazil. This marks the first high-profile gathering of the "greater BRICS family" in its new "11+10" format - comprising 11 member countries and 10 partner countries - following Indonesia's official entry into the BRICS cooperation mechanism in January and Vietnam's official joining as a BRICS partner country in June. The summit is themed "Strengthening Global South Cooperation for More Inclusive and Sustainable Governance." As the host country, Brazil has outlined three key priorities for the meeting: deepening cooperation in public health, promoting a unified stance on climate change, and establishing mechanisms to facilitate trade and investment among member states. On the eve of the summit, Colombia and Uzbekistan formally joined the New Development Bank as full members. Today, the BRICS family represents over half of the world's population, accounts for one-fifth of global trade, and contributes nearly 30 percent of global GDP. This remarkable momentum is no accident - it reflects the growing appeal of the "BRICS spirit" of openness, inclusiveness, and win-win cooperation. According to data from the International Monetary Fund (IMF), in 2024, BRICS collectively reached 4 percent GDP growth, significantly outpacing the global average. This demonstrates that the "greater BRICS" has become a "southern engine" that continuously fuels global development.

According to some foreign media outlets, this year's summit will discuss important topics, including the establishment of a new guarantee fund and the "Tropical Forests Forever Facility," and will voice collective positions on IMF reform. As the world is entering a new period of turbulence and transformation, characterized by rising unilateralism and protectionism, and some major powers increasingly disengaging from international governance, BRICS remains steadfast in its original aspiration, focusing squarely on cooperation and development. All its agendas and agreements are being gradually implemented, turning words on paper into real development outcomes. As of 2024, the BRICS New Development Bank has approved 120 projects worth a total of $39 billion, covering key sectors such as transport infrastructure, clean energy, healthcare, and social development. As the "vanguard of the Global South," the "greater BRICS" governance proposals are receiving global attention, and the world is looking to the "greater BRICS" for wisdom and contributions.

The growing influence of the "Greater BRICS" is evident in Western reporting. From the very start, the Rio BRICS Summit has become a focal point of global attention. Reuters noted that the expansion of the "Greater BRICS" "has added diplomatic weight to the gathering" and the bloc is presented "as a defender of multilateralism in an increasingly fractured world." The New York Times focused on the new role of "BRICS" in global governance, emphasizing its ambition to "rebalance global power dynamics." Although some media outlets maintain a "critical" and "skeptical" attitude toward the BRICS Summit, the inherent "traffic appeal" of the Rio Summit is enough to reflect the international community's attention to and recognition of BRICS.

The BRICS countries differ in terms of historical culture, political systems, economic size, and development levels, and there are differences between overall interests and individual interests. However, this precisely reflects the valuable inclusiveness and complementarity of the BRICS mechanism. BRICS cooperation is a systematic collaboration of the Global South; it is both comprehensive cooperation and open-door cooperation. It embodies the voices of the Global South, providing more development opportunities and equal rights for countries in the Global South, and promoting an equal and orderly multipolar world as well as a universally beneficial and inclusive economic globalization. This not only aligns with the interests of the Global South but also contributes to the common good of the world.

From promoting the establishment of the New Development Bank to advocating for the "BRICS+" cooperation model; from articulating the "four major partnerships" among BRICS countries to building new industrial revolution partnerships within BRICS, China's contributions to the BRICS mechanism are evident. According to the "Hand in Hand: China-LAC Mutual Perception Survey," released by the Global Times Institute during the "Global Times' Overseas China Week and Global South Dialogue" series of events held in Latin America in late June, a majority of respondents from six Latin American countries believe that the BRICS can represent the Global South to voice its concerns on the international stage. Furthermore, 93 percent of Latin American respondents believe that China has brought opportunities for development to the region, and 84 percent recognize China's development prospects. Through its own actions, China has built a bridge of hope for common development, making the gears of "greater BRICS" cooperation operate more smoothly.

IIn the face of the ever-changing international landscape, BRICS countries have demonstrated strong cohesion and action, providing a "BRICS answer" to the changes unseen in a century, which enhances the credibility of BRICS. The Rio Summit will mark a new starting point. Looking ahead, BRICS countries will continue to uphold the "BRICS spirit," deepen cooperation in various fields, promote reforms in the global governance system, and make greater contributions to world peace and development.- Global Times

BRICS is not “against” anything; it is “for”: for the development, for a fairer world order, and a larger role for the Global South. It concentrates on specific development problems, which makes BRICS very attractive to other developing

"We face serious and existential challenges at regional and international levels, a matter that necessitates consensus among major countries. We count on this economic bloc (BRICS) to be a voice for the Global South and developing countries," said Egyptian Foreign Minister Badr Abdelatty in an interview with Russia Today.

The collective rise of the Global South is a distinctive feature of the great transformation across the world. Today the Global South represents over 70 percent of the world's population and more than 40 percent of the world's Gross Domestic Product. But they are relatively under-represented on the world stage. BRICS, which recently held its 16th Summit in Kazan, Russia from Oct 22 to 24, stands at the forefront of the Global South focusing on pooling collective wisdom to open up new prospects for development and prosperity for all developing countries.

At the summit, China called on BRICS to uphold peace, strive for common security and common prosperity and promote the flourishing of all civilizations. These proposals respond to the Global South's urgent need for peace, development and cooperation, and are consistent with China's Global Development Initiative, the Global Security Initiative and the Global Civilization Initiative.

China will always be a member of the Global South. Solidarity and cooperation with fellow developing countries is the unshakable foundation of China's foreign relations. China believes that global modernization should be pursued through the joint efforts of all countries, in a way that promotes peaceful development and mutually beneficial cooperation bringing prosperity to all. This goal is consistent with China's vision of building a community with a shared future for mankind.

China's announcement is matched with concrete actions and tangible outcomes. Over the years China has provided development assistance to over 160 countries, conducted development cooperation with more than 150 countries involved in the Belt and Road Initiative, energized cooperation with more than 100 countries, the UN and many other international organizations under the Global Development Initiative, provided nearly US$20 billion of development funds and carried out over 1,100 projects. China's steady contribution to the development of the Global South has empowered the construction of an equal and orderly multipolar world.

Through the concerted efforts of China, Brazil, Russia, India and South Africa, BRICS countries have successfully expanded their ranks by welcoming new members. This year's summit marks the start of the "Greater BRICS Cooperation". China also proposed the "BRICS Plus" cooperation model. During the Kazan Summit, more than 20 leaders or representatives of invited guest countries from Asia, Africa, Europe and Latin America and heads of six international organizations attended the "BRICS Plus" Leaders' Dialogue. The BRICS mechanism is now widely regarded as an inclusive platform for development and growth. It is fundamentally different from the closed-door clubs run by some countries bearing all the marks of rigid Cold War mentalities and bloc confrontation.

China made this commitment at the summit that it will always keep the Global South in its heart, and maintain its roots in the Global South. When members of the Global South pull together, great power will be unleashed for their own people's well-being and for all humanity living in our community with a shared future.— China Daily/ANN

By Zhu Qing , The author is a commentator on international affairs. The views don't necessarily represent those of China Daily.

Dedollarise move: a file picture of us banknotes. Economists say there are incentives to move away from using the greenback as the primary currency for trade settlement and reserves.

— afp

THE US-dollar dominance as the anchor of the international financial system is being challenged on several fronts simultaneously – and ever more intensely – in recent months.

From several countries opting to conduct trade in their local currencies, instead of using the US dollars to the BRICS nations of Brazil, Russia, India, China, South Africa seeking to develop a new common currency for the economic bloc, the risk of the mighty greenback being dethroned appears serious.

As some economists say, it is no longer a question of “if” the US dollar’s dominance will crack, but “when”. Is this a good thing for small and open economies like Malaysia?

According to economists, there are incentives to move away from using the US dollar as the primary currency for trade settlement and reserves.

Bank Muamalat Malaysia Bhd chief economist and social finance head Mohd Afzanizam Abdul Rashid points out that the high dependence on the US dollar will make the global economy highly susceptible to changes in the US monetary policy.

The move to dedollarise will not only reduce financial-market volatility caused by US monetary conditions, but it can also help reduce costs, he says.

Afzanizam explains: “Any change in the US monetary policy will affect the global financial market. This is a problem, as it can sometimes create excessive volatility in foreign-exchange markets.”

“Because of this, companies and investors have to hedge their exposure to mitigate currency risks. Hedging is cost to businesses and investors. Therefore, the incentives to do away with the US dollar is high,” he says.

Afzanizam tells Starbizweek if there were currencies that could provide better alternatives in terms of stability and predictability, dedollarisation would certainly gain further traction.

According to Sunway University economics professor Yeah Kim Leng, dedollarisation, that results in improved global economic and financial stability leading to increased trade and investment flows, will be beneficial to small and open economies like Malaysia.

“As a trading nation, pragmatic and nimble government and company-level policies and strategies are vital to cope with the potential fallouts and opportunities arising from dedollarisation that may or may not lead to a more stable and progressive global economic order,” he explains.

Cost and benefit

Malaysia is seen to be moving towards dedollarisation. Early this month, the country reached a deal with India, one of its major trading partners, to settle trade in Indian rupees instead of the US dollar.

In addition, Malaysia revived the idea of setting up an Asian Monetary Fund (AMF), proposing to initiate discussions on the matter with China, which is reportedly open to the idea.

These small steps are part of an ongoing global shift away from US dollar dependence.

Socio-economic Research Centre executive director Lee Heng Guie says there are potential costs and challenges during the transition process.

“Malaysia may face heightened exchange rate volatility if the dedollarisation is disorderly and abrupt, causing a plunge in the US dollar against major foreign currencies. The wide and deep US dollar fluctuations could impact trade, investment and capital flows,” the economist explains.

For example, a sharp appreciation of the ringgit against the US dollar could lower the cost of servicing Malaysia’s Us-dollardenominated debt, but it could dampen the country’s export competitiveness and lower exchange rate translation gains in domestic currency for the export-oriented industries such as palm oil, rubber products and crude petroleum.

“Portfolio investors may undertake portfolio adjustment in anticipation of the dedollarisation. This could induce assets price fluctuations in the debt and equities markets as investors stay on the sidelines, while assessing the potential risks and costs associated with a disorderly transition of the dedollarisation,” Lee says.

Lee: the wide and deep us dollar fluctuations could impact trade, investment and capital flows.

Regardless of the transition costs and risks, Malaysia has to continue strengthen its domestic financial markets, enhance policy credibility, and foster regional and multilateral cooperation in the provision of liquidity arrangement.

“The development of deep and liquid domestic financial markets is a prerequisite for buffering against the impact of dedollarisation,” he says.

Meanwhile, Malaysia University of Science and Technology economics professor Geoffrey Williams sees two basic scenarios pertaining to dedollarisation.

Williams: the use of the us dollar will slowly decrease.

“The first is that the use of the US dollar will slowly decrease, as more countries settle trade and investment in bilateral currencies. This will continue as BRICS and smaller countries get onboard.

“The second scenario is that there will be a tipping point where the US dollar will quickly lose reserve currency status as happened to pound sterling after World War II. There are many possible triggers of this, but they are very speculative and involve a major crisis,” he adds.

Williams says the United States will defend the dollar and so long as the dollar is used for oil, metals and commodity trades as well as intergovernmental settlement of debt, it will retain its role.

Gradual transition for stability

It is estimated that the US dollar accounts for 88% of global trades, based on Bureau for International Settlements’ triennial central bank survey 2022.

As it stands, central banks around the world still hold significant amounts of US dollars in their reserves. An estimate by the International Monetary Fund implied that the greenback accounted for about 60% of global foreign exchange reserves as at end2022.

Nevertheless, economists expect the numbers to be on a declining trend, as countries are diversifying away from the US dollar. The dedollarisation process, however, will likely be gradual to minimise disruption to global financial systems and markets.

As Afzanizam puts it, any abrupt transition to other currencies can create uneasiness and uncertainties among businesses and investors.

Therefore, allowing ample time would facilitate the changes and reduce the inevitable market volatility, he says.

The enormous and deep US debt markets have been touted as a major factor for the continuing dominance of the US dollar in global financial markets, according to Yeah.

Yeah: the yuan is expected to see a rising role as one of several alternatives.

Therefore, as countries diversify their reserve currencies and reduce dependence on the US dollar, one could expect global financial markets to face higher volatility and uncertainty, he says.

On Malaysia’s effort to wean off US dollar dependence, Yeah points out that it will be a gradual process.

“This will be in line with global shifts in international trade, capital flows and financial markets, whereby the process is driven by market forces and factors such as transaction costs, riskiness, accessibility and convenience,” he says.

As a start, Malaysia can consider trading its oil and other natural resources in local currencies with countries with which it has bilateral agreements, says HELP University economist Paolo Casadio.

Further, he notes, Malaysia can have a meaningful and impactful transition towards less reliance on US dollar by coordinating its effort with other economic blocs, such as BRICS, to set up a new system.

“There are long-term benefits for Malaysia as well as for all the other developing countries in eliminating the (US dollar) monopoly,” Casadio says, pointing to a more stable and equitable exchange rate as an example.

Asian fund proposal

On the setting up of the AMF, Williams says while it is a feasible strategy to reduce reliance on the US dollar, such a move will require “buy-in” across many countries in the region. In particular, pertinent issues such as who will to provide the finance, and securing consensus on the terms on which access to that finance is made available, have to be ironed out.

“It is not just a financial issue, but geopolitical too,” he stresses.

“The main issue is who will fund it, and what will be the contribution rates for each member. It is likely that most will come from China, unless Japan and South Korea join in. Otherwise, most Asian countries are too small to contribute much,” he adds.

Williams says new arrangements, such as the 12-member Comprehensive and Progressive Agreement for Trans-pacific Partnership, of which Malaysia is a part, are indications of ongoing shifts in global economic arrangements away from dominance of the United States and other developed economies such as the European Union (EU).

“Moving to bilateral currencies for trade and investment is feasible, but more at risk to exchange fluctuations and liquidity issues. So, it would be a move to multiple currency options, not just one,” he says.

He notes before US or Eu-based systems such as the Society for Worldwide Interbank Financial Telecommunication, or SWIFT, could be replaced, there has to be a viable and reliable alternative for interbank transfers and e-payments.

“Although the systems are contestable and replaceable by new and local providers, the truth is that only stable, reliable and secure financial systems will survive. The US dollar still provides this,” Williams argues.

Importantly, for Malaysia as a small country, it should go with the flow and remain neutral in the shifting geopolitical dynamics, while trade and debt, in whatever currency is best, he says.

Potential alternatives

Amid the ongoing currency shift, China’s yuan, is increasingly seen a potential alternative to the US dollar. This is by virtue of China being the second-largest economy in the world after the United States. However, the country’s strict capital controls are a hindrance.

“As the world’s second-largest economy, China’s yuan is expected to see a rising role as one of several alternatives, including the euro, to the US dollar. Countries trading with China are already increasingly using yuan for payments and settlements,” Yeah says.

“Its internationalisation, however, is being constrained by strict capital controls and lack of liquidity for international transactions outside of China,” he adds.

Concurring with Yeah, Afzanizam says, for the yuan to play an even greater role as an alternative international currency, China’s capital account has to be more open, allowing free flow of funds to allow greater flexibility, especially in terms of the supply of yuan.

Casadio, on the other hand, argues there is no alternative to the US dollar in the prevailing system.

Rather, a “gold-backed system of currencies that constitutes an alternative” is a more viable option, this will provide an equitable system of exchange rates and a stable international financial system, he explains.

“There is a clear shift, at the international level, towards a system in which the dollar has no more monopolistic power as the international currency. The system that is going to emerge from this will limit monopolies and excess financing deficits, thanks to it being anchored to gold,” says Casadio.

Charles Schwab Corp says that there aren’t any viable reserve-currency alternatives to the US dollar.

“A reserve currency needs to be freely convertible and have deep and liquid bond markets to be considered safe for foreign central banks to hold. Central banks need to know that their money is easily and readily available when needed, particularly in times of stress.

“The United States, with a large, open, and liquid market for Treasury securities, fits that role,” the investment bank explains in its commentary.

“That’s why when the Covid crisis hit the global economy, the US Federal Reserve (Fed) expanded its swap lines with foreign central banks to enable access to dollars for countries that were struggling to access dollars for trade and debt payments. While other major countries’ markets have these qualities, the size and openness of the US market is difficult to match,” it adds.

Depreciating dollar

In the meantime, the US dollar is expected to weaken further against most currencies through the year on anticipation of slower interest rate hikes by the Fed.

The greenback has already been on a declining trend over the past few months. This is evidenced by the downtrend of the US dollar index - a gauge of its performance against a basket of major currencies - with the DXY falling to around 100 to 102 points from its multi-year high of 114 to 115 points in September 2022.

From the Malaysian perspective, the ringgit has been volatile against the greenback.

The local note is trading RM4.43 against the US dollar. This is an improvement from RM4.75 in early November last year, but a poorer position from RM4.24 at end-january this year.

With the expected weakening of the US dollar, the ringgit is forecast to strengthen to RM4.15-RM4.25 towards the second half of this year, says Dr Yeah.

“The US economy is anticipated to weaken significantly in the second half and that could warrant unwinding the high interest rates,” he explains.

Similarly bearish on the greenback, Afzanizam says he expects the ringgit to strengthen to RM4.20 against the US dollar by the end of 2023.

“The expectation of slower rate increase in the United States and the potential cut in the federal fund rate could lead to a weaker US dollar,” he explains.

Although on a decline, the US dollar’s dominance is expected to persist due to the absence of a viable alternative.

“The pace of its decline, however, could accelerate if US economic growth sputters, fiscal and debt woes mount and high inflation and interest rates destabilise its banking system.

“Continuing US economic instability coupled with the government’s penchant to apply sanctions for geopolitical reasons will also motivate the rest of the world to band together to find a viable alternative while reducing dependence on the dollar for trade, financing and foreign reserves,” he adds.

The United States' way of weaponising the dollar to control global trade is losing ground and more and more

countries are shying away from using the greenback. — Reuters

The US dollar system will be dominant for a while yet, but the more the dollar is weaponised in terms of sanctions, the more users will want to dedollarise. — Reuters

How does BRICS continually play its role in the world?

It's been 16 years since the foundation of the BRICS mechanism was laid. China hopes to work with all BRICS countries to respond to the major concerns of the international community and build a more comprehensive, closer, more practical and inclusive partnership. Even more, China hopes to keep its promises to the 2030 Agenda for Sustainable Development Goals.Against current risks and challenges, the participants also pledged to ensure that the customs authorities of BRICS countries continue to work together to safeguard the international supply chain and promote rapid economic and trade recovery among BRICS countries. In this upcoming episode of "The Chat Room", we talk about how does BRICS continually play its role in the world. Also, focusing on the member states' achievements and challenges under BRICS, we invite five guests from BRICS countries to share their opinions. How does Sino-Indian cooperation play its role in the world? What's the current economic situation of BRICS? What roles has BRICS found itself in the world? How should we see BRICS+ in the future? #BRICS2022

China's Xi Slams Sanctions for 'Weaponizing' World Economy at BRICS

BRICS-led New Development Bank approaches 7th anniversary

China will host the 14th BRICS Summit on June 23 and Chinese President Xi Jinping will join with the leaders of Brazil, India, Russia and South Africa via video link to discuss issues of mutual concern as part of the summit themed around ushering in a new era for global development. The New Development Bank, established in 2015 by the BRICS countries, will soon celebrate its 7th anniversary. Tian Wei talks to the bank's Brazilian president Marcos Troyjo about his visions for the multilateral institution.#BRICS2022

Aerial photo taken on June 17, 2022 shows the headquarters building of the New Development Bank (NDB), also known as the BRICS bank, in east China's Shanghai.(Photo: Xinhua)

In a keynote speech at the opening ceremony of the BRICS Business Forum on Wednesday, Chinese President Xi Jinping called on the BRICS business community to expand cooperation on cross-border e-commerce, logistics and local currencies.

As the 14th summit of the BRICS, a group of major emerging market economies comprising Brazil, Russia, India, China and South Africa, kicked off on Wednesday, there are growing calls from bankers and economists in BRICS countries, especially Russia, for the bloc to expand national currency settlements and lending to counter the US' weaponization of the dollar.

Russian President Vladimir Putin said in a welcome address to BRICS Business Forum participants on Wednesday that the issue of creating an international reserve currency based on a basket of currencies is under review, Russian news agency TASS reported.

"The BRICS and other interested nations need to talk about setting up their own independent global financial system - whether it would be based on the Chinese currency or they will agree on something different. They need to debate this," Sergey Storchak, chief banker of Russian bank VEB.RF, told the Global Times in a video interview on Tuesday.

Storchak said that he hopes during China's presidency of this year's BRICS summit, member countries have open discussions on what really needs to be done.

VEB.RF is a major financial development institution in Russia that has been excluded from the SWIFT system.

There has been an ongoing discussion within the BRICS to accelerate payments in national currencies for years, and the need is becoming particularly urgent after the US removed some Russian banks from the SWIFT global interbank payments system and forced other economies to pay for its economic problems with sizeable financial tightening.

"If the voices of emerging markets are not being heard in the coming years, we need to think very seriously about setting up a parallel regional system, or maybe a global system," he said.

The impact of being pushed out of the SWIFT system is quite large, Storchak said. "The biggest issue is the transfer of money and information, and we need to come to the issue of the wide utilization of national currencies. It would mean that we would not need to use the banking system of either the US or the EU," he said.

Such calls for an independent payment system are growing within the BRICS.

Marco Fernandes, a Brazil researcher at the Tricontinental Institute for Social Research, also called on the BRICS to focus on creating an alternative to the US dollar's hegemony in global transactions at a conference at the Chongyang Institute for Financial Studies of the Renmin University of China on Tuesday.

"After confiscating tens of billions of dollars in reserves and assets from countries like Iran, Venezuela and Afghanistan, the seizure by the US and the EU of more than $300 billion of Russia's reserves, triggered a global alert, reaffirming the urgency of alternatives to the dollar's dominance," Fernandes said.

Analysts noted that the US' increasing use of the dollar as a political weapon in recent years - through sanctions or conditional loans - prompts countries to seek other currencies for commercial transactions and in the composition of their foreign reserves.

To shrug off pressure from the US to join in its sanctions against Russia, India was exploring the possibility of using the Chinese yuan as a reference currency in an India-Russia payment settlement mechanism for its oil trade with Russia, Indian news outlet Livemint reported in May.

In addition, former Kremlin economic adviser Sergey Glazyev has proposed a new global financial system - via an association between the Eurasian Economic Union and China - that would be underpinned by digital currency and backed by a basket of new foreign currencies and natural resources of the member countries, according to website The Cradle, which mainly covers West Asian geopolitics.

Cao Heping, an economist at Peking University, said that there are other bilateral or multilateral global settlement systems for cross-border financial services, including China's Cross-border Interbank Payment System (CIPS).

The CIPS processed around 80 trillion yuan ($11.91 trillion) in 2021, up more than 75 percent year-on-year. According to data from SWIFT, the yuan retained its position as the fifth most active currency for global payments by value in April, with a share of 2.14 percent.

Cao suggested that BRICS members step up cooperation in investment and financing in major sectors such as strategic emerging industries and digital innovation in a bid to boost the use of local currencies in trade and investment settlement.

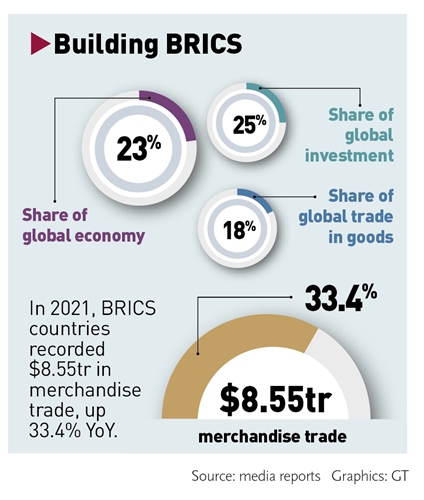

BRICS countries are an important driving force for regional and global economic and trade growth. Despite the prolonged impact of COVID-19, the total volume of trade in goods of BRICS countries reached nearly $8.55 trillion in 2021, up 33.4 percent year-on-year, official data showed.

The bloc accounts for 18 percent of trade in goods and 25 percent of foreign investment globally, statistics show.

"Along with the development of the mobile internet, digital payment has also become a tool for cross-border transactions. More opportunities are expected in this regard," Cao said.

Negative rates: Pedestrians walking

past the Bank of Japan (BoJ) headquarters in Tokyo. BoJ’s goal remains

at keeping real interest rates as negative as possible, as long as the

economy performs. — Bloomberg

IT’S mid-term review time as the US yield curve begins to flatten.

This curve tracks the relationship between interest rates of US government debt obligations. Normally the yield curve is rising, with long-term bonds having yields higher than short-term obligations.

But occasionally the curve inverts, with long bonds yielding less than short Treasury bills – a historical predictor of future recessions and bear markets in stocks. Recently, the curve has become noticeably flatter, with short rates rising and longer yields remaining stagnant. This has led many analysts to think that the yield curve will soon invert.

But that does not mean a recession is imminent. Just returned from an extended visit back to Harvard. Touched base with my mentors and professors at both extremes of the economic spectrum. They are all split on what this flattening really means. In the event it does invert (the gap today being below 0.3%), recession has almost always (over the past 50 years) followed within a year or so. But few see a recession soon on the horizon.

The first half has come and gone. The ongoing transition to more normal conditions continue in the context of a robust US economy; continued progress in the orderly normalisation of US monetary policy; and re-awakened sensitivities to geopolitical and protectionist risks.

There will be higher interest rates, some inflation concerns and trade tariffs coming-on in the context of markets more readily accepting two to three more rate hikes by the Fed in 2018. The prospect of a global trade war makes everyone very cautious.

Once we start down the road of tariff increases and threats of more to come, the dangers of retaliatory miscalculations are real and very scary. Still even an inverted yield curve should not be on top of our worry list under today’s accommodative monetary conditions.

Synchronised pick-up

The world economy benefitted from four drivers of higher growth: the healing process in Europe, re-bound from slowdowns in Brazil, India and Russia; soft landing in China; and pro-growth measures in US.

To persist, Europe needs to do much more. Also, there is hope that recent tariff tensions would eventually lead to fairer and still-free trade which recognises the inter-dependent nature of global supply chains, and show greater willingness to protect intellectual property rights, modernize trade arrangements and reduce non-tariff barriers. Yes, more rate hikes from the Fed are still on the cards. But the same by the European Central Bank (ECB) and Bank of Japan (BOJ) demand trickier manoeuvring.

This is an area that warrants close monitoring since volatility will likely persist. At least for now, fears of Japan-like deflation in US and Europe are effectively gone. But OECD is worried global growth is not yet self-sustaining. It’s strength in 2018 is largely due to monetary and fiscal policy support – and lacking in rising productivity gains and sweeping structural reforms. In Europe, the “clock is ticking”; without reforms, more populist uprisings will appear as the upswing ages and then fades. US inflation is not only returning to the Fed’s 2% target, but also likely to exceed it. In Europe, consumer prices were last still lower than a year ago – below the ECB’s target of just below 2%. Fear of the spectre of deflation has led BOJ to remain cautious about tapering its monetary easing program. Will just have to wait and see.

IMF warns that the world’s US$164 trillion debt pile (at 225% of GDP) is bigger than at the height of the financial crisis a decade ago. One-half was accounted for by US, Japan and China. What’s needed is for US fiscal policy to be recalibrated to bring down the government debt to GDP ratio (80%) and for China to deleverage its US$ 2.6 trillion private debt. There is no sign either is being done which runs the risk of triggering yet another financial crisis.

Growth will falter

Growth in US can slow considerably when the boosts from last year’s tax-cuts in US fades in 2019 and 2020. IMF now warns that US will grow at about one-half the 3% annual pace forecast by the White House over the next 5 years, reflecting the effects of growing massive fiscal deficit and continuing trade imbalance. For US, sluggish productivity remains a key determinant. In 2Q18, GDP picked-up to rise 4.1% (2.2% in 1Q18) the fastest pace in nearly four years, reflecting broad-based momentum.

But worker productivity advanced 1.3% from a year earlier, consistent with the sluggish 1.2% average annual rate in 2007-2017, well below the better than 2% annual average since WWII. Spending by consumers, businesses and government as well as surging exports all appeared solid in 2Q18. The expansion enters its 10th year this month, building on what is already the second longest expansion on record. Faster growth which has helped to drive the unemployment rate to its lowest level in 18 years, fueled quick corporate profit growth.

Median estimates place GDP growth at 2.8% in 2018, 2.4% in 2019 and 1.8% over the long run. But everyone has growth slowing next year because of falling business and consumer sentiment, reflecting trade disputes with China and many US allies, and uncertainty whether rising business investment is sustainable.

The big concern is the economy overheating – already, it is bumping up against capacity constraints as labour markets tighten. Still, the consensus is that the next downturn will not arrive until 2020. Most economists expect 3% inflation over the next year. What worries me most is the deteriorating global political and strategic environment.

Not so much the economic outlook directly. The world is changing too much, too fast.

So much so, the geopolitical situation is getting worse – open warfare between Israel and Iran, the disgraceful state of Palestine, and uncertainties surrounding Donald Trump and Vladimir Putin, and lack of leadership in Europe. Trade barriers are causing much anxiety. It is as though what’s put in place since WWII isn’t worth a damn anymore.

Europe and Japan

Latest indications from the Brookings-FT Index for Global Economic Recovery (Tiger) show global growth has peaked and momentum has started to fade. Indeed, financial markets are already reflecting mounting vulnerabilities. With weak economic data in 1H’18, Europe and Japan have since cooled. In late 2017, eurozone was still growing at 3.5%: Germany at 4%, France 3%, Italy 2% and Spain 3.5%. But activity slackened to only 1.2% in early April; even Germany recorded a sharp dip – down to only 1%, reflecting waning monetary easing effects and supply-side constraints. The outlook is for a strong above trend upswing for the rest of the year. OECD now expects GDP growth in 2018 to be 2.2% (2.6% in 2017) and in 2019, 2.1%.

For eurozone, the window for reforms is closing – ranging from the implementation of dual currencies for its members to putting European Parliament in charge of economic policy, including the euro-budget. Japanese GDP shrank 0.1% in 1Q18 despite a rise in capital investment. Household spending unexpectedly fell. Still, recovery is expected to be driven by a weak yen brought about by monetary stimulus (BoJ has been buying assets at US$740 billion a year to drive down long-term interest rates). But underlying inflation is stuck at 0.5%. BoJ’s goal remains at keeping real interest rates (after inflation) as negative as possible, as long as the economy performs. OECD forecasts growth in Japan to be 1.2% in 2018 (1.7% in 2017); the same in 2019.

China and BRICS

Many emerging markets (EMs) are still enjoying momentum from 2017, but there is growing concern about rising debt and vulnerabilities to capital flight as interest rates in US rise. For those recently emerged from recession, viz. Russia, Brazil and South Africa, their urge to return to strong levels of activity remains sluggish.

China and India have fewer concerns for their immediate outlook. Still, they need to reform their economies to help raise living standards to catch up. The main challenges will be to execute particular reforms – not just to the financial system but also to SOEs and local governments, including getting rid of corruption.

China’s GDP rose 6.7% in 2Q’18, the slowest pace since 2016. Retail sales held up rather well as did exports. Still, measures to curb rampant borrowing are biting – investments in infrastructure and manufacturing by SOEs and local governments have since slackened. These efforts, in the midst of headwinds from abroad (especially protectionist tariffs), have led to downgrades in growth for the rest of the year. IMF now forecasts GDP growth in China to average 6.5% in 2018 (6.8% in 2017) and about the same in 2019.

Recent depreciation of China’s currency, the yuan, exposes crucial vulnerabilities within the world’s second-largest economy as it faces escalating trade tensions with the US. The currency posted its biggest ever monthly fall against US$ in June (3.4%) and has since lost more ground. This slide marks a departure for the currency often regarded as an anchor of stability for Asia and other EMs.

As Beijing assesses the options, it finds itself between a rock and a hard place because (i) People’s Bank of China (PBoC) intervention means selling its US dollar stash of reserves – which stood at US$3.11 trillion in June; (ii) it could instead raise domestic interest rates, thereby making the currency more attractive which might help to shore up the yuan. But it also risks weakening an already slowing Chinese economy just as the trans-Pacific trade war starts to bite; and (iii) it could impose stricter controls on China’s capital account which will likely spook overseas funds that have rushed into China’s domestic bond and equity markets this year at an unprecedented rate.

However, to internationalise the yuan, China has to keep fund flows relatively unencumbered. The PBoC has sensibly pledged to keep the RMB “generally stable.” In July, China implemented a mix of tax cuts and greater infrastructure spending citing growing uncertainties, as it ramps up efforts to stimulate demand to counteract a weakening economy.

As for India, I wrote extensively on what’s happening there (my July 2018 column: “India: Chugging Along but Needs More Firepower” refers).

What then are we to do

As I see it, China and China-India centred Asia is now the heart of the world economy. Their steady growth has been a source of stability in an otherwise unsteady world.

Of late, developments in China received more scrutiny than usual because of the context: Chinese stock market has since fallen into bear territory, and a growing trade dispute with the world’s largest economy, US. Despite China’s astonishingly sustained expansion, the economy is widely considered vulnerable because growth in output has been underwritten by an even faster increase in debt.

The nation’s gross debt – both public and private – is now estimated at over 250% of GDP. The worry is not just the volume of debt but its quality. China’s domestic policies encourage high savings.

Those savings, held in banks, have been funneled to companies, especially SOEs. The credit quality of the loans is hard to assess but is likely to be uneven. China has since begun to slowly tighten the credit taps, with even tighter rules on shadow banking and more scrutiny for both local government financing and public-private investment projects.

At the same time, a sharp increase in the number of defaults by corporate issuers has revived anxieties about Chinese debt. In my view, it is the tighter credit conditions and defaults, rather than worries about a trade war, that best explain the recent 22% decline in the Shanghai Composite index from its January highs.

Tightening credit policy is also a compelling explanation for the weak macro-economics. Credit growth fell, and growth in fixed investment followed. This appears to be having some effect on consumer sentiment as well.

No doubt, Trump’s tariffs on US$50bil of Chinese imports (and threatens US$200bil more) will have a direct (but unlikely to be catastrophic) impact on growth. But China is now an investment-led rather than an export-led economy.

Still, it is the knock-on effects that are most feared. If the escalation of hostilities leads to a reduction in foreign direct investment in China, the long-term impact could be significant. True, China may be facing a delicate moment economically.

But given China’s deepening role in the world economy, any pain that the US manages to inflict on it would be quickly shared with the US and the broader world – at a moment when Europe’s economy is slowing, and many EMs looking unstable.

On the whole, China’s economy will remain strong and resilient. Whatever happens, I think this won’t change the Chinese situation much.

By Lin See-yan - what are we to do?

Former banker Tan Sri Lin See-Yan is the author of The Global Economy in

Turbulent Times (Wiley, 2015) and Turbulence in Trying Times (Pearson,

2017). Feedback is most welcome.